Backcharge Cost Breakdown Template and Calculator

AI/Search Snippet: This backcharge cost breakdown template and calculator helps construction teams enter dated remedial-cost items, calculate quantity × rate, apply one clearly named adjustment or credit, and print or export a structured cost summary. The calculation supports a backcharge record but does not itself establish liability or create a right to deduct money from payment.

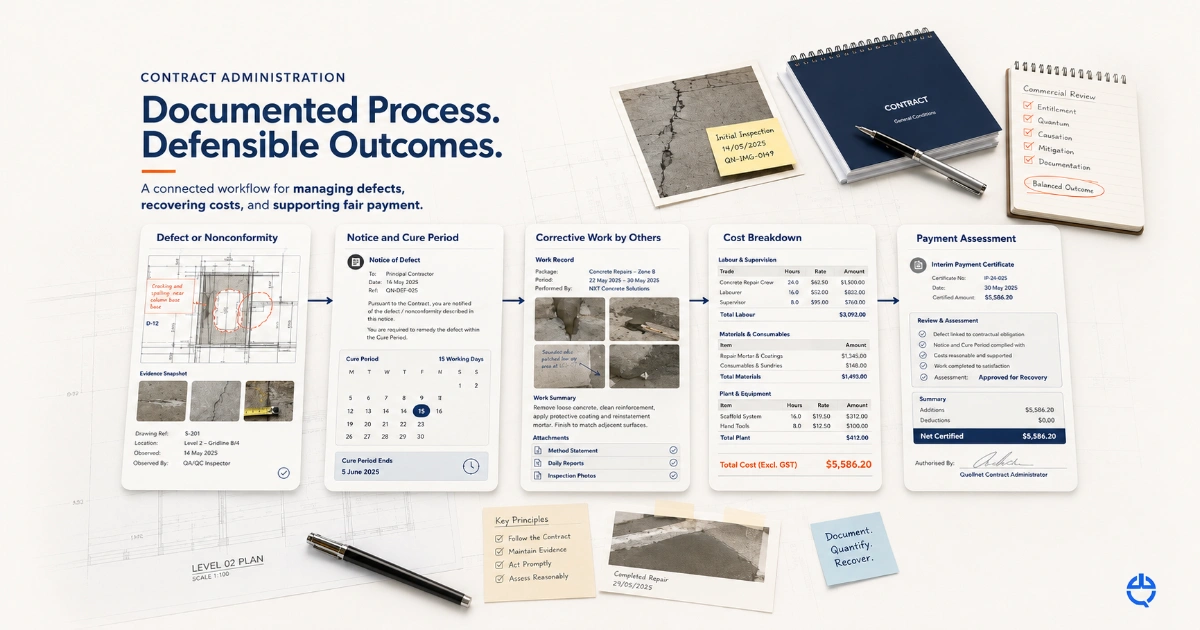

A backcharge cost breakdown template is the itemized numerical record behind a proposed construction backcharge. It explains how the claimed amount was calculated and connects each labour, material, plant, specialist, testing, or access cost to the corrective work performed.

The calculation is only one part of the process. Before cost recovery is pursued, the charging party should establish the contractual failure, identify the responsible party, provide any required instruction or notice, allow the applicable correction opportunity, and follow the relevant claim and payment procedures.

For the wider contractual framework, see the main guide to backcharges under construction contracts.

What Is a Backcharge Cost Breakdown?

A backcharge cost breakdown is a dated and itemized record of the reasonable cost allegedly caused by defective, incomplete, damaged, delayed, or noncompliant work.

It should be distinguished from the other documents used in the process:

- Notice to Correct: requires the responsible party to remedy a stated failure within an applicable period.

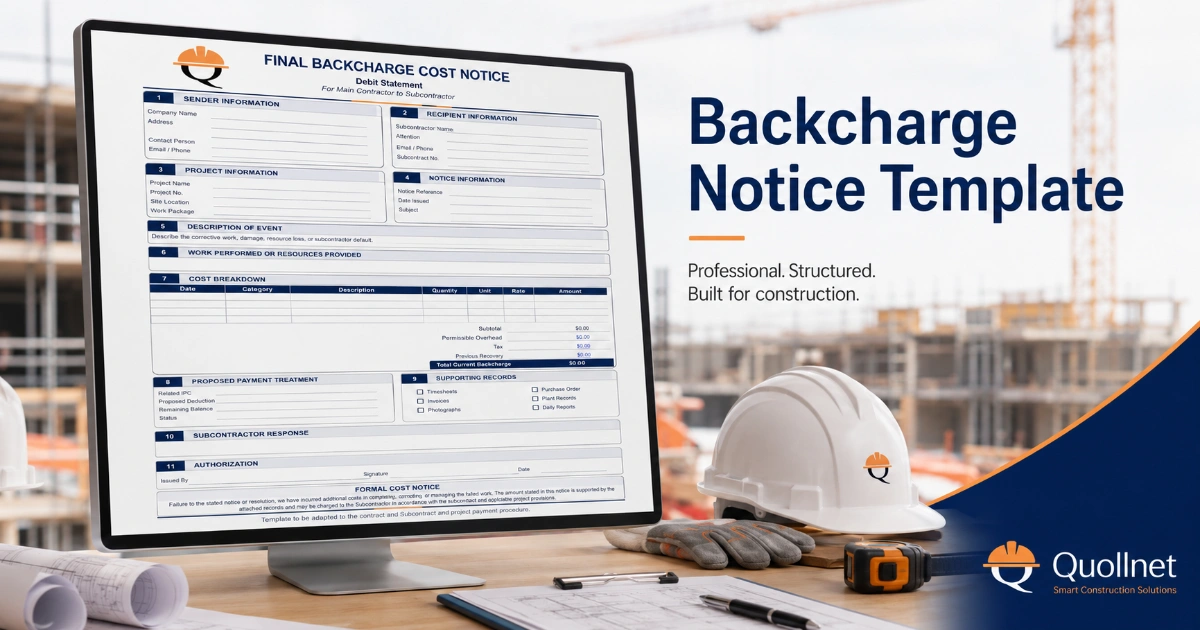

- Initial Backcharge Notice: warns that correction by others and cost recovery may follow.

- Final Backcharge Cost Notice: presents the supported actual or contractually assessed amount.

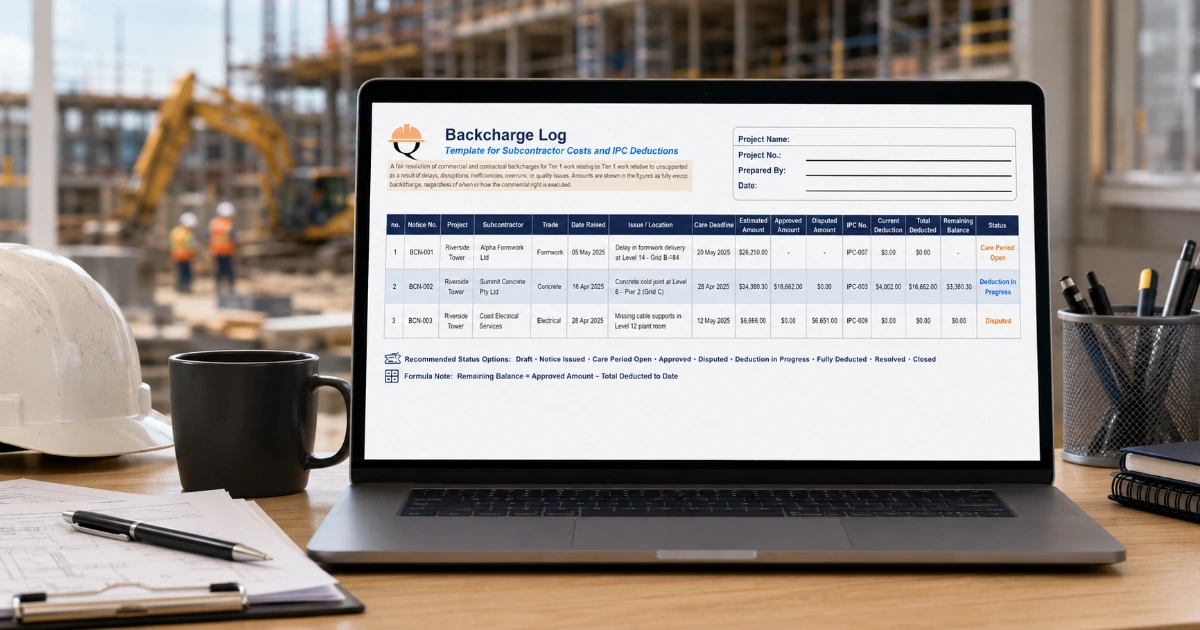

- Backcharge Log: tracks notices, estimates, deductions, balances, disputes, and closure across the project.

- IPC deduction: shows the amount applied to a particular Subcontractor payment.

The notice establishes the alleged failure and correction opportunity. The cost breakdown records the reasonable cost allegedly resulting from that failure.

Use the Backcharge Cost Breakdown Calculator

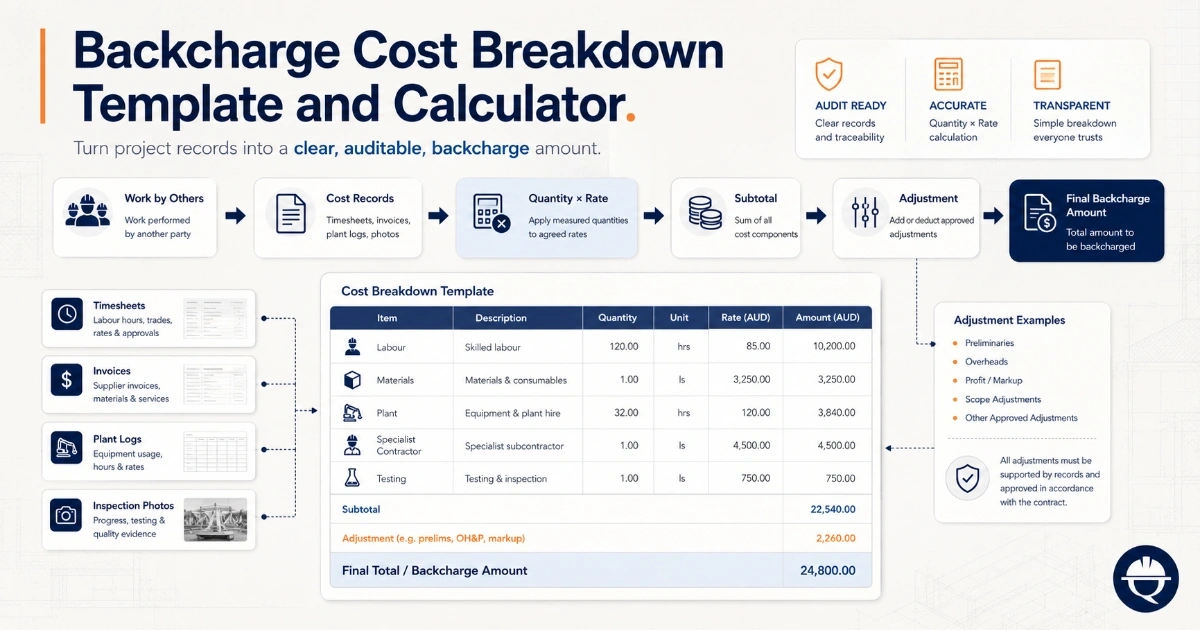

Enter each remedial-cost item below. The calculator multiplies quantity by rate, totals the cost rows, and allows one named adjustment such as supervision, overhead, tax, discount, or credit. The completed summary can then be printed or exported for review and attachment to the project record.

Backcharge Cost Breakdown Calculator

Add dated cost items, calculate quantity × rate, apply one named adjustment, and export a clear construction backcharge cost summary.

Record information

Optional details for reports and exports.

Show optional project and record fields

Cost items

Amount is calculated as quantity multiplied by rate.

| Date | Description | Category | Quantity | Rate | Amount | Row actions |

|---|

Subtotal

-

Total

-

This calculator prepares an administrative cost breakdown only. It does not establish liability, validate a backcharge, or create a contractual right to deduct the amount from payment. Verify the applicable notice, correction, claim, approval, and payment procedures.

Contractual disclaimer

This calculator prepares an administrative cost breakdown only. It does not establish liability, validate a backcharge, or create a contractual right to deduct the amount from payment. Verify the applicable notice, correction, claim, approval, assessment, and payment procedures.

Where corrective work is still only proposed, mark the calculation as an estimate or quotation. Do not present the total as an agreed debt or final deduction before the required work, records, contractual assessment, and payment procedure have been completed.

What Should Be Included in the Cost Breakdown?

Each cost category should be supported by a record showing what was used, when it was used, why it was necessary, and how it relates to the original failure.

Labour

Record the date, trade or operative, hours worked, applicable rate, and corrective activity. Supporting evidence may include signed timesheets, daily reports, payroll records, attendance sheets, or an approved labour allocation.

Materials

Identify the material, quantity, unit, rate, supplier, and affected repair. Attach supplier invoices, delivery notes, material issue vouchers, purchase orders, or stock records. Credit unused or returned material where appropriate.

Plant and Equipment

State the plant item, duration, operating or hire rate, and purpose. Support the amount with hire invoices, plant logs, allocation records, delivery tickets, or agreed internal rates.

Specialist Contractor

Record the company performing the correction, the instructed scope, quotation, purchase order, invoice, and completion evidence. The specialist’s work should be limited to reasonable correction rather than unrelated improvement.

Testing and Inspection

Include necessary reinspection, laboratory testing, commissioning, surveys, specialist reports, or verification of the repair. Link the cost to the relevant inspection requirement or Inspection and Test Plan.

Access, Protection, Removal, and Disposal

Necessary access towers, permits, temporary protection, opening up, removal, disposal, and reinstatement may be recorded where they were reasonably required to perform the correction.

Other Supported Cost

Use this category cautiously. Describe the cost clearly, identify the supporting document, and explain why it does not belong in another category. Avoid using “other” to hide unsupported administration, unrelated preliminaries, or a general commercial allowance.

Quantity × Rate Is Not Enough

A numerical calculation can be arithmetically correct and still be contractually unsupported. Each line should also record:

- the date the cost arose;

- a clear description of the work or resource;

- the cost category;

- the source record or document reference;

- why the cost was necessary;

- how it relates to the original defect or default;

- whether it is estimated, quoted, committed, or actual;

- whether it has been reviewed, agreed, determined, or disputed.

For example, “16 hours × 35” does not explain who performed the work, what was corrected, whether the hours were reasonable, or whether the rate includes an additional markup.

The breakdown should also identify the original site instruction, NCR or defect record, and the relevant Notice to Correct.

Estimated, Actual, Approved, and Agreed Costs

Cost status should be shown explicitly. An estimate should never become a final IPC deduction merely because the same amount has been carried forward for several months.

| Status | Meaning |

|---|---|

| Estimate | Preliminary value prepared before corrective work is performed. |

| Quotation | Third-party price offered but not necessarily instructed or incurred. |

| Committed cost | Amount covered by an instruction, work order, or purchase order but not yet finally invoiced. |

| Actual cost | Cost supported by invoices, timesheets, plant records, or other completed-work evidence. |

| Internally approved | Amount accepted through the issuing organisation’s internal review. |

| Agreed | Amount accepted by both contractual parties. |

| Determined | Amount assessed, certified, or determined under the contract procedure. |

| Disputed | Amount challenged in whole or in part. |

| Final | Closed amount used for the final project and payment record. |

Internal approval is not the same as agreement by the recipient. Likewise, a supplier invoice proves that a cost was charged to the issuing organisation, but it does not automatically prove that the whole amount is recoverable from the Contractor or Subcontractor.

How to Use the Single Adjustment Field

The calculator provides one named adjustment field that can be used for an addition or a credit.

Possible adjustment labels include:

- Supervision

- Contractually permitted overhead

- Administration

- Tax or VAT

- Discount

- Credit

- Insurance recovery

- Other adjustment

The adjustment should be transparent. State its name, contractual or accounting basis, and calculation. Use a negative amount for a discount, credit, returned material, insurance recovery, or amount already recovered elsewhere.

Do not automatically add overhead or profit. Confirm whether the executed contract or subcontract permits it and whether the particular cost-recovery mechanism includes that item.

Avoid combining several unrelated amounts inside one adjustment. If the total contains supervision, tax, a discount, and an insurance credit, prepare a separate supporting calculation showing each component.

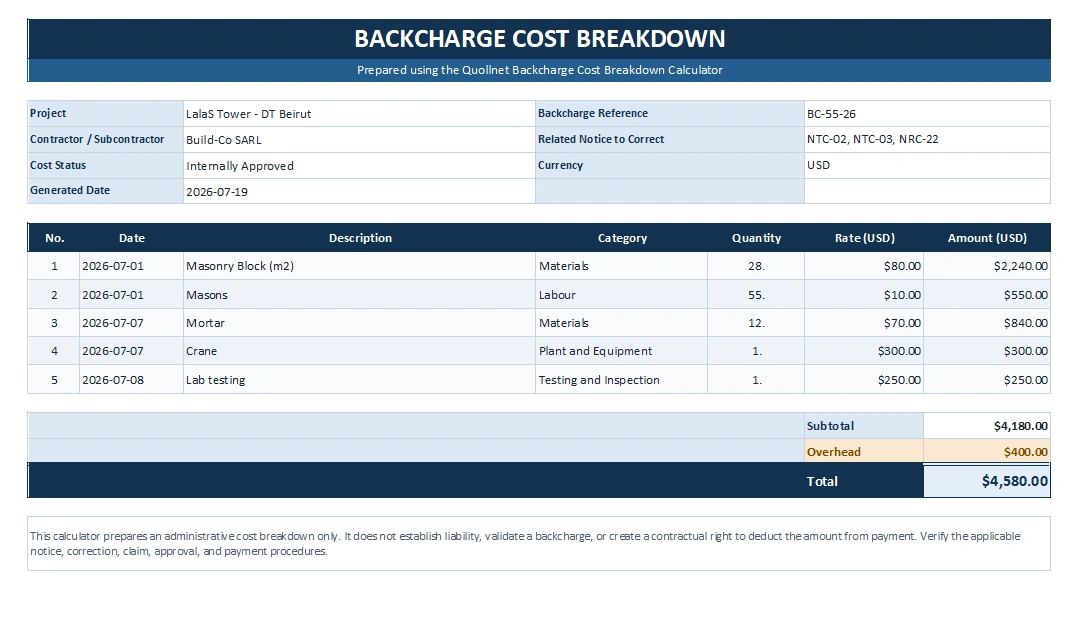

Worked Backcharge Cost Example

An electrical Subcontractor fails to correct noncompliant cable supports after receiving notice and access. The Main Contractor records the following corrective work performed by others:

| Date | Description | Category | Quantity | Rate | Amount |

|---|---|---|---|---|---|

| 18 Jul 2026 | Two electricians completing corrective work | Labour | 16 hr | 35 | 560 |

| 18 Jul 2026 | Replacement cable supports | Materials | 1 lot | 275 | 275 |

| 19 Jul 2026 | Mobile access tower | Plant | 1 day | 140 | 140 |

| 19 Jul 2026 | Reinspection of corrected installation | Testing | 1 visit | 180 | 180 |

Subtotal: 1,155

Named adjustment—necessary supervision: 75

Total proposed backcharge: 1,230

The labour line should be supported by timesheets identifying the electricians, dates, hours, and work performed. The material amount should be linked to the supplier invoice or stock issue. The access tower requires a hire invoice or plant record, and the reinspection should be supported by the inspection request, report, or specialist invoice.

The supervision adjustment should identify the time spent, the person involved, why that supervision was additional, and the contractual basis for recovery.

Costs That May Be Challenged

The recipient may accept that corrective work was necessary while disputing part of the cost.

Common objections include:

- betterment or upgraded materials;

- replacement of compliant adjacent work;

- unnecessary demolition or replacement scope;

- excessive labour hours;

- premium, overtime, or emergency rates that could have been avoided;

- inefficient working methods;

- unsupported supervision;

- overhead or profit without contractual entitlement;

- unrelated work or management cost;

- duplicate labour, invoice, or plant entries;

- damage caused by another trade;

- cost increased because access was denied or notification was delayed;

- insurance proceeds, rebates, returns, or credits not deducted;

- estimates presented as final actual cost.

Where the corrective work includes an upgraded specification, redesigned system, increased quantity, or other improvement, separate the cost of restoring compliance from the additional element. The additional work may be a Variation or betterment rather than a recoverable correction cost. See Managing Variation Orders.

The charged party can use the itemized schedule to challenge unsupported backcharge costs without denying legitimate responsibility for reasonable correction.

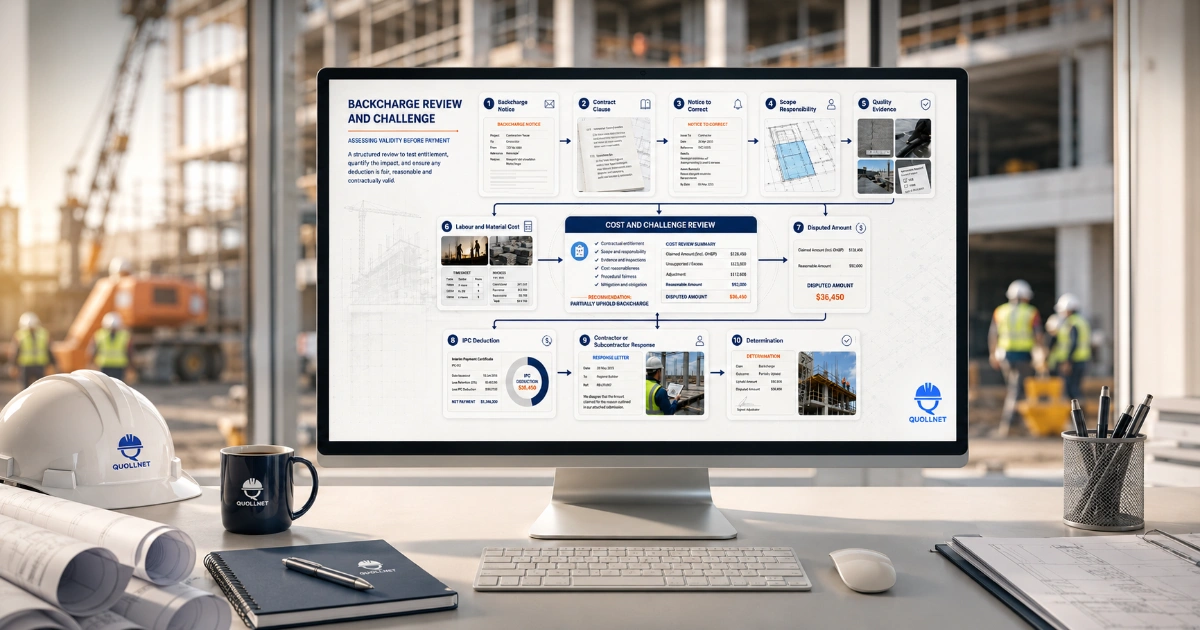

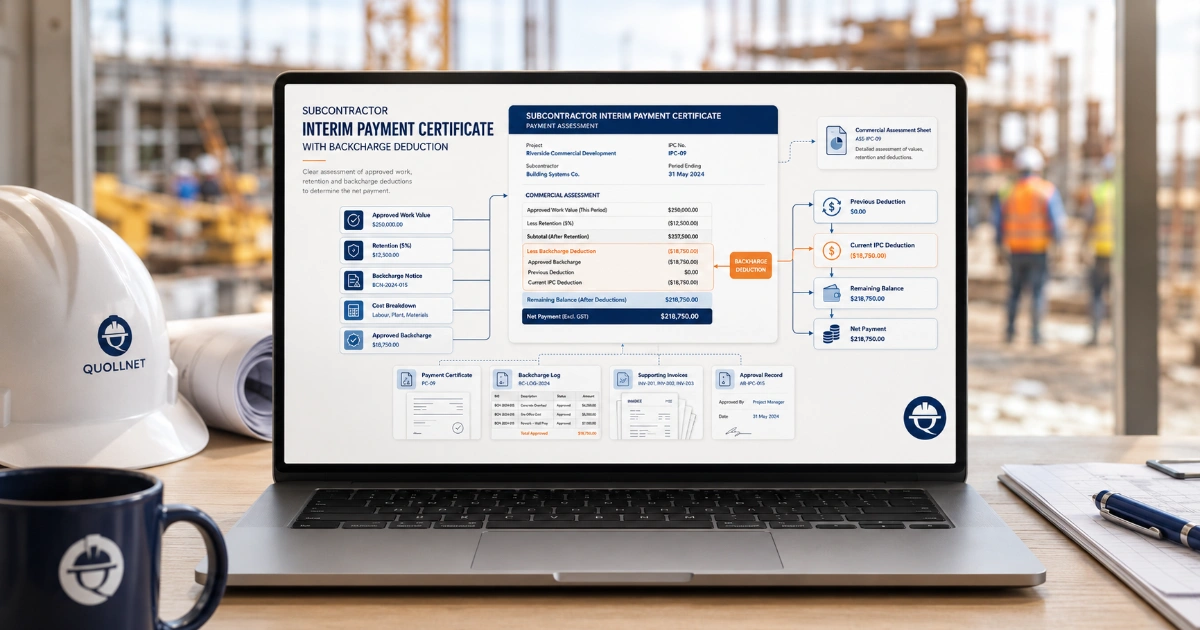

From Cost Breakdown to Payment Deduction

A completed calculation should not move directly into an IPC without checking the contractual sequence.

- Confirm the failure and contractual responsibility.

- Confirm that the required instruction, defect notice, or Notice to Correct was issued.

- Confirm that access and the applicable correction opportunity were provided.

- Record the actual corrective work and supporting documents.

- Prepare the cost breakdown and assign the correct status to each amount.

- Issue the Final Backcharge Cost Notice or contractual claim.

- Record the amount in the Construction Backcharge Log.

- Obtain any required agreement, assessment, certification, determination, or internal approval.

- Apply the contractual payment, set-off, or pay-less notice procedure.

- Show the approved current deduction and remaining balance in the Subcontractor IPC.

The total cost breakdown and the current IPC deduction may differ. For example, the supported cost may be 10,000 while only 4,000 is deducted from the current payment, leaving a clearly recorded balance of 6,000. Part of the amount may also remain disputed, provisional, or subject to later assessment.

The detailed entitlement varies under FIDIC, AIA, NEC4, and JCT. Check the relevant guide before presenting the amount as immediately deductible.

Supporting-Record Checklist

- Executed contract or subcontract and relevant clause

- Site instruction

- Notice to Correct

- Initial Backcharge Notice

- NCR or defect record

- Photographs and marked-up drawings

- Specifications and acceptance criteria

- Inspection and test records

- Access records

- Recipient’s response

- Labour timesheets

- Material invoices and delivery notes

- Plant records and hire invoices

- Specialist quotation, work order, and invoice

- Testing or reinspection report

- Internal commercial approval

- Final Backcharge Cost Notice

- Payment Notice or Pay Less Notice

- Backcharge Log reference

- IPC deduction schedule

Final Practical Note

A transparent cost breakdown makes a backcharge easier to review, approve, challenge, adjust, and close. It does not replace the contractual procedure, but it provides the numerical and documentary basis needed for that procedure.

Record estimates separately from actual costs, disclose every adjustment, apply all credits, and retain a clear connection between each cost line and the corrective work. Where the responsible party was entitled to inspect or repair, also preserve the notice, access, and correction-period records.

This calculator and article provide general construction contract-administration support and are not legal advice. The executed contract or subcontract, amendments, governing law, payment legislation, tax treatment, and project facts control.

REFERENCES

FIDIC: Determination of Costs Following Failure to Remedy Defects

FIDIC Construction Contract, Second Edition 2017, Reprinted 2022

AIA Contract Documents: Owner’s Right to Carry Out the Work

AIA Contract Documents: Rejection and Correction of Work

NEC: Defining and Managing Defects and Liability for Not Correcting Them

NEC: Dealing with Uncorrected Defects under the ECS