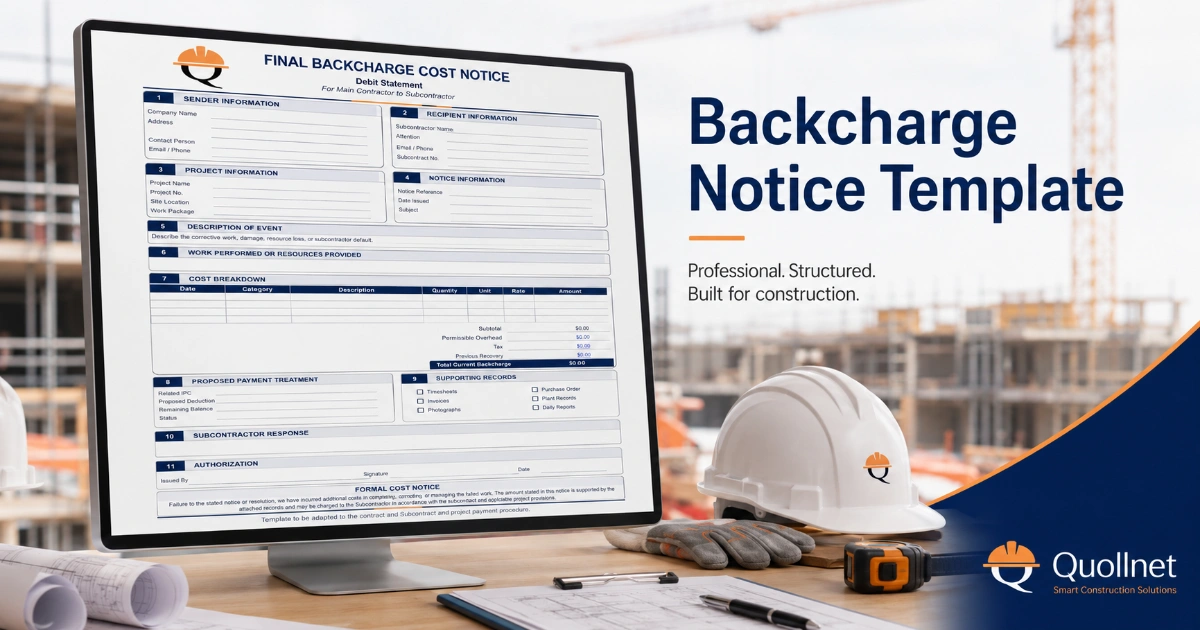

Backcharge Log Template for Subcontractor Costs and IPC Deductions

A backcharge log tracks each proposed or confirmed Subcontractor backcharge from the initial notice and cure period through cost assessment, approval, dispute, IPC deduction, reversal, and closure. The log separates estimated, approved, disputed, deducted, and remaining amounts to support an auditable commercial record and prevent duplicate payment deductions.

Need the log now?

Download and Use the Backcharge Log below to track notices, cure periods, cost assessments, approvals, disputes, IPC deductions, and remaining balances. Each entry should be supported by the relevant notice and cost records before it is treated as an approved payment deduction.

Contractual caution: A Backcharge Log is an administrative control record. Entry in the log does not by itself establish liability, approve the cost, or create a contractual right to deduct a backcharge from a Subcontractor’s payment.

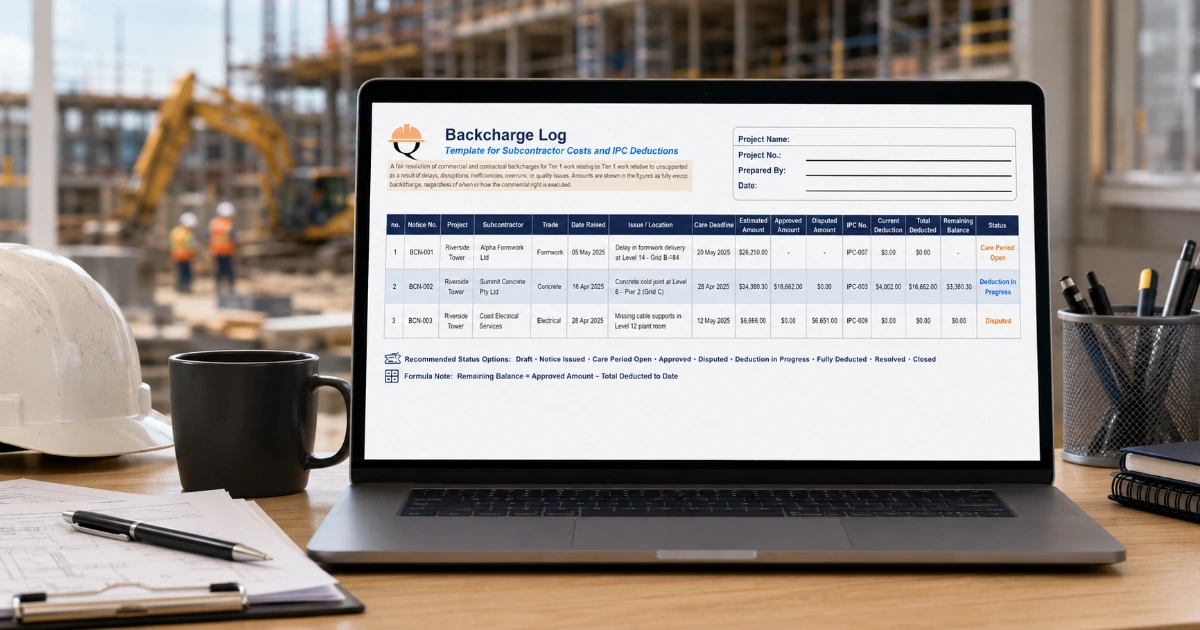

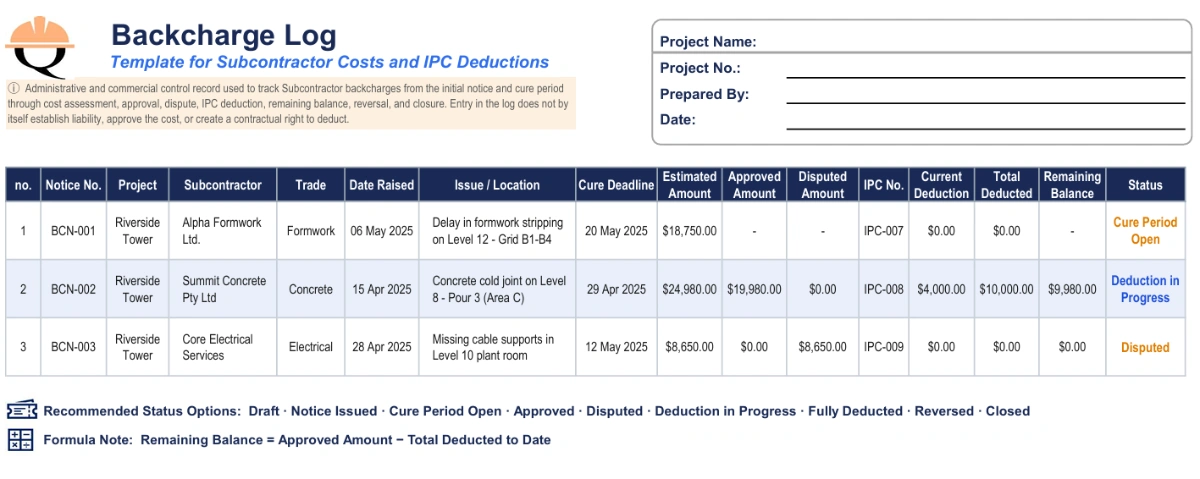

Core Construction Backcharge Log Template

The following core log is designed for normal project use. It contains the fields needed to identify the backcharge, monitor the cure period, separate the financial amounts, and reconcile each deduction with the relevant Subcontractor interim payment certificate.

The sample entries are illustrative only.

| Serial | Notice No. | Project | Subcontractor | Trade / Package | Date Raised | Issue / Location | Instruction / NCR | Cure Deadline | Cure Status | Estimated Amount | Actual Cost | Approved Amount | Disputed Amount | IPC No. | Current IPC Deduction | Total Deducted | Remaining Balance | Status | Remarks / Record Reference |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | BCN-001 | Riverside Tower | Alpha Formwork Ltd. | Formwork | 6 May 2026 | Delayed stripping, Level 12, Grid B1–B4 | SI-146 / NCR-087 | 20 May 2026 | Open | $18,750 | — | — | — | — | $0 | $0 | $0 | Cure period open | Initial notice issued; no cost approved. |

| 2 | BCN-002 | Riverside Tower | Summit Concrete Pty Ltd. | Concrete | 15 April 2026 | Cold-joint remedial work, Level 8, Pour 3 | SI-132 / NCR-071 | 29 April 2026 | Expired | $24,980 | $21,240 | $19,980 | $0 | IPC-11 | $4,000 | $10,000 | $9,980 | Deduction in progress | Approved under CA-044; previous deduction in IPC-10. |

| 3 | BCN-003 | Riverside Tower | Core Electrical Services | Electrical | 28 April 2026 | Missing cable supports, Level 10 plant room | NCR-079 | 12 May 2026 | Disputed | $8,650 | $8,650 | $0 | $8,650 | — | $0 | $0 | $0 | Disputed | Subcontractor denies responsibility; no deduction approved. |

For larger projects, an extended Backcharge Register may also include the Subcontract number, relevant clause, responsible team member, payment-notice reference, internal approval history, Subcontractor response, supporting-document link, accepted amount, closure date, and reversal history.

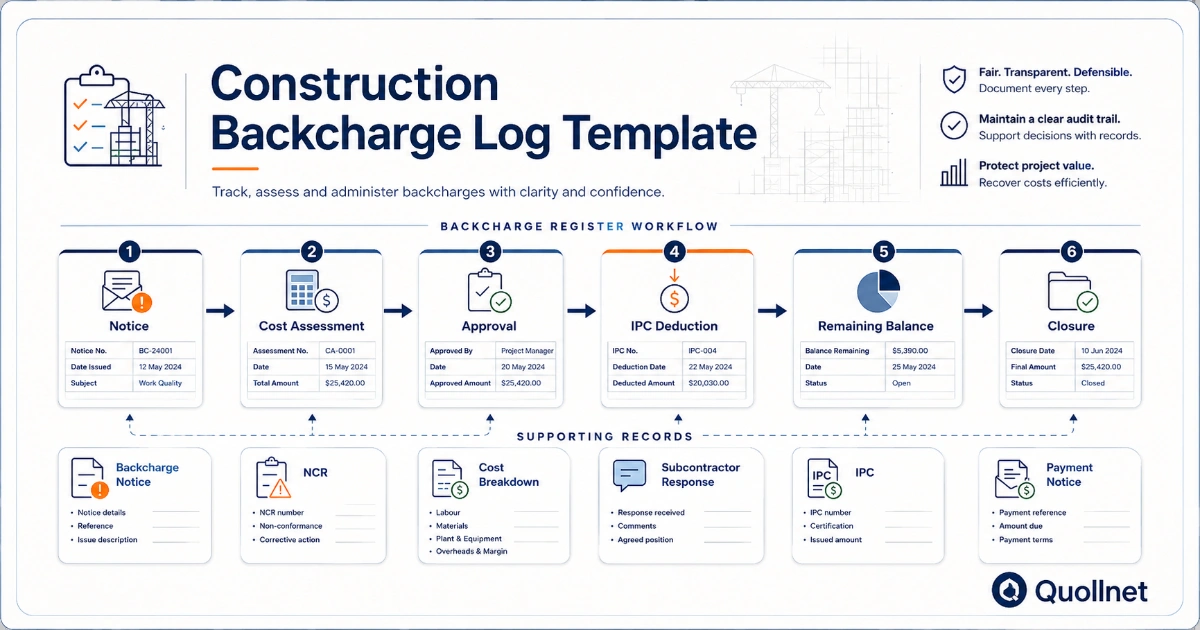

What a Backcharge Log Tracks

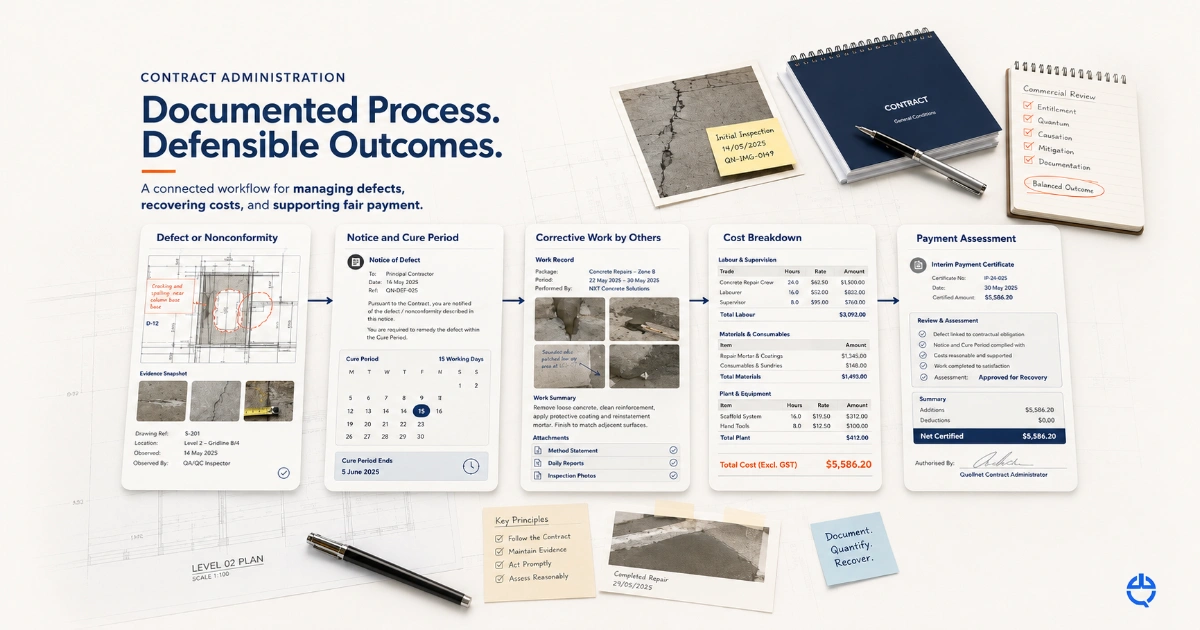

A Backcharge Log connects the technical event to its commercial and payment consequences. The record normally begins when a defect, omission, damage event, delay-related issue, or failure to comply is identified and a notice is raised.

The entry should then follow the matter through the cure period, Contractor intervention, cost assessment, internal review, Subcontractor response, approval, payment deduction, and closure. The status must describe the current commercial stage—not merely whether the original technical defect remains open.

For example, the physical work may already have been corrected while the cost remains under assessment or disputed. In that case, the technical record may be closed while the Backcharge Log remains open.

Recommended Backcharge Status Options

| Stage | Recommended statuses |

|---|---|

| Notice and cure | Draft, Notice issued, Cure period open, Rectified by Subcontractor, Contractor intervention required |

| Cost assessment | Cost pending, Under assessment, Submitted for approval, Approved, Partially approved |

| Response and dispute | Disputed, Partially accepted |

| Payment | Deduction pending, Deduction in progress, Fully deducted |

| Closure | Reversed, Withdrawn, Closed |

Do not delete withdrawn, reversed, or rejected entries. Retaining them in the register preserves the audit history and explains why an amount shown in an earlier report no longer appears in the Subcontractor’s payment assessment.

Key Financial Fields in a Backcharge Register

The financial columns must distinguish between a preliminary estimate and an amount that is ready for payment treatment:

- Estimated amount: the initial forecast before the remedial work and supporting costs are complete.

- Actual cost: the recorded labour, material, plant, specialist, and other recoverable cost supported by project records.

- Approved amount: the amount authorized under the project’s commercial approval procedure.

- Disputed amount: the amount challenged or not accepted by the Subcontractor.

- Current IPC deduction: the amount included in the current payment assessment.

- Total deducted to date: the cumulative amount deducted in all previous and current IPCs.

- Remaining balance: the approved amount that has not yet been deducted.

Remaining balance = Approved amount − Total deducted to date

Do not calculate the remaining balance from an estimated or disputed amount.

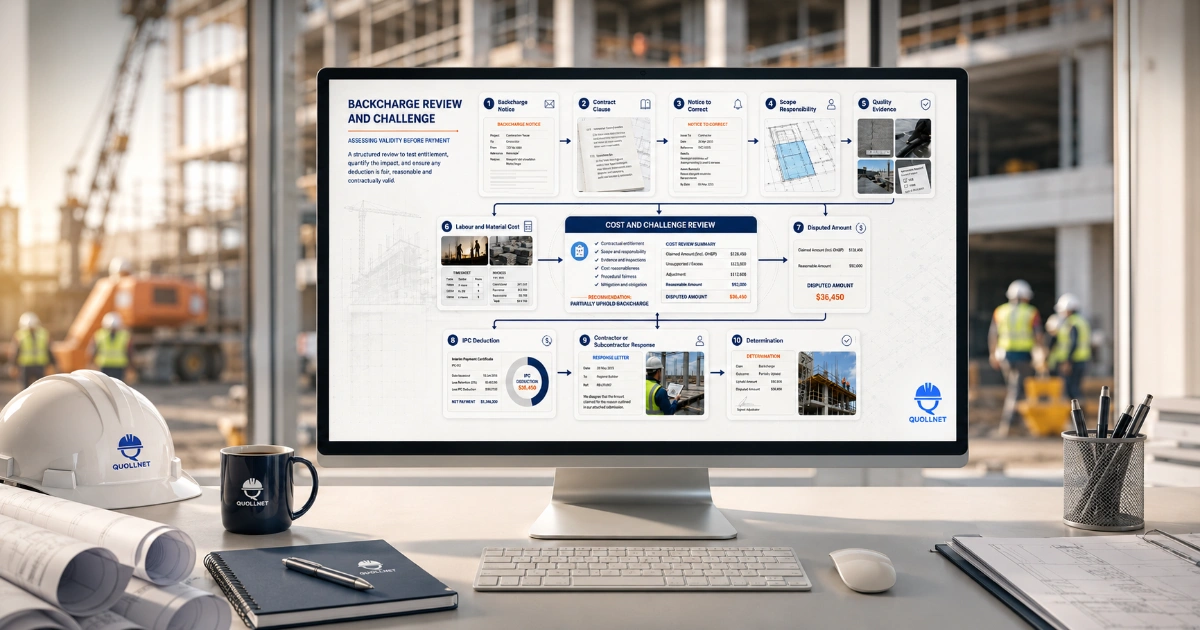

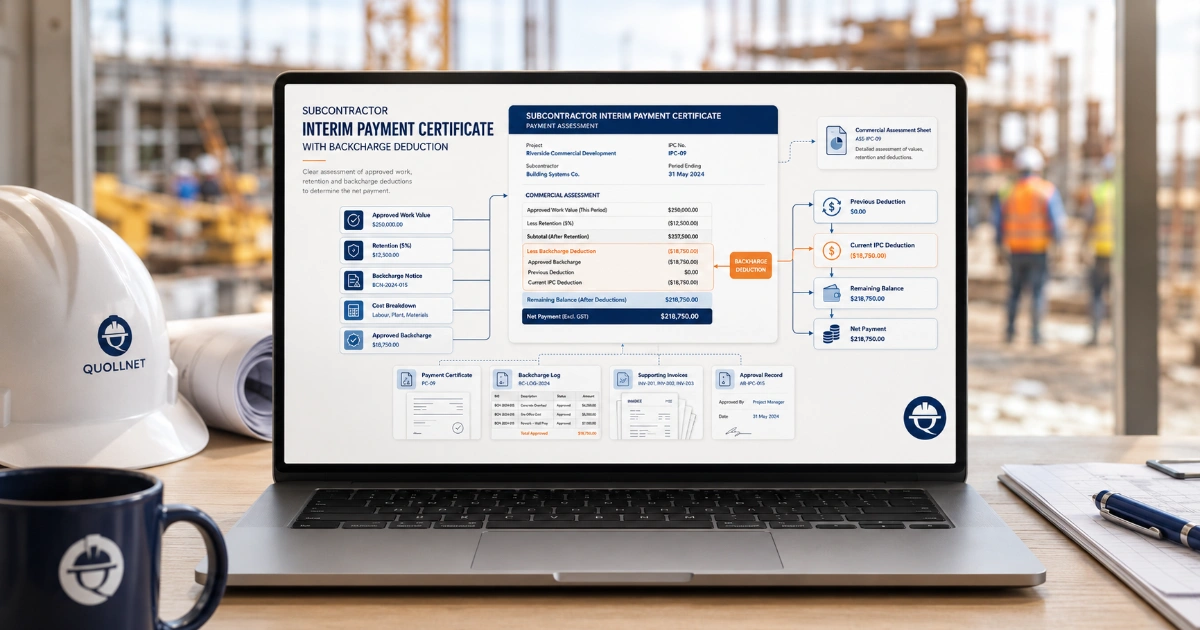

Linking the Backcharge Log to the Subcontractor IPC

The most important control is a consistent Backcharge Notice number. The same reference should appear on the initial notice, final cost notice, Backcharge Cost Breakdown, Backcharge Log, Subcontractor IPC deduction line, payment notice or pay-less notice, and final account record.

The log must show both the total approved amount and the total deducted to date. This prevents the same approved amount from being deducted in full more than once.

For example:

- Approved backcharge: $12,000

- Deducted in IPC 10: $5,000

- Deducted in IPC 11: $4,000

- Remaining balance: $3,000

The next IPC should therefore deduct no more than the remaining $3,000 unless the approved amount is formally revised. The commercial team should also record any later credit, reversal, settlement, or reduction against the same notice reference.

Before adding a line to the IPC, verify the applicable contractual procedure, issue the required Backcharge Notice, substantiate the amount, and record the approved deduction in accordance with the project’s Subcontractor IPC assessment procedure.

Backcharge Log Versus NCR Log

An NCR Log tracks a technical nonconformity, its cause, corrective action, inspection, and closure. A Backcharge Log tracks commercial cost recovery, approval, dispute, and payment treatment.

A single nonconformance report may be rectified without producing any backcharge. Conversely, one backcharge may combine costs arising from several NCRs, photographs, instructions, labour records, or specialist invoices.

The two registers should be linked by reference number but should not be treated as the same document.

Supporting Documents and Backcharge Controls

Each entry should link to the records needed to explain the event, responsibility, cost, approval, and payment treatment:

- Backcharge Notice and Notice to Correct.

- Site instruction and related correspondence.

- NCR, photographs, inspection records, and daily reports.

- Labour timesheets, plant records, material invoices, and specialist quotations.

- Cost breakdown and internal commercial approval.

- Subcontractor response or dispute notice.

- Relevant IPC page and payment notice or pay-less notice.

- Settlement, reversal, withdrawal, or closure record.

Before closing each monthly IPC, the quantity surveyor or commercial manager should confirm that:

- estimated and actual costs are recorded separately;

- the deduction does not exceed the approved amount;

- previous deductions have been carried forward;

- the remaining balance is mathematically correct;

- disputed amounts are not presented as approved deductions;

- credits and reversals have been entered; and

- retention and backcharges remain separate payment items.

Common errors include recording only the original claim, changing the notice number between documents, repeating the deduction across several IPCs, leaving rectified notices open, failing to record reversals, and treating entry in the register as proof of liability.

Contract-Specific Backcharge Guidance

The correct notice, cure, assessment, certification, and deduction procedure depends on the Subcontract and governing law. For contract-specific explanations, refer to the Quollnet guides for FIDIC backcharges, AIA backcharges, NEC backcharges, and JCT backcharges.

A Subcontractor disputing an unsupported, duplicated, or procedurally defective deduction should preserve its notices, payment records, supporting evidence, and contractual objections. See the guide on how to challenge an improper construction backcharge.

REFERENCES

Backcharges in Construction Contracts

Construction Backcharge Notice Template

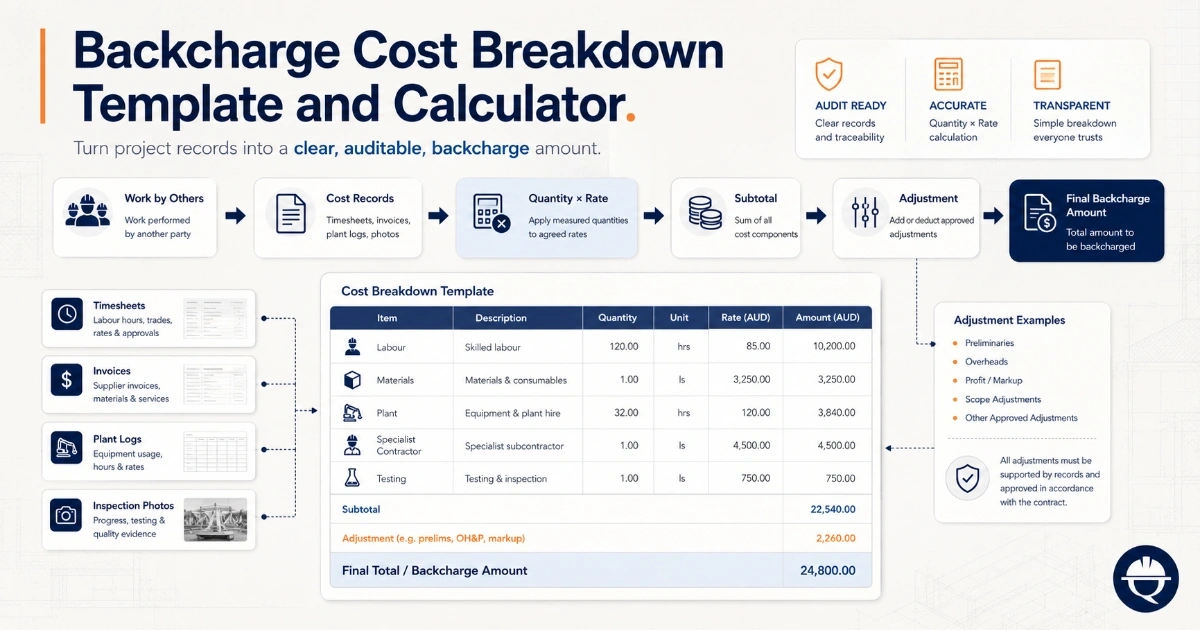

Backcharge Cost Breakdown Template and Calculator

Backcharge Deduction from a Subcontractor IPC

Timely Notices in Construction

AIA: Managing the Contingency Allowance

FIDIC: Works of Civil Engineering Construction—Contemporary Records and Substantiation

AIA Contract Documents: Construction Payment and Project Record Forms