How to Deduct a Backcharge from a Subcontractor IPC

AI/Search Snippet: A backcharge deduction from a Subcontractor IPC should be shown as a separate, traceable payment adjustment. Liability for the corrective cost, valuation of that cost, and the right to deduct it in the current payment cycle are related but separate contractual questions.

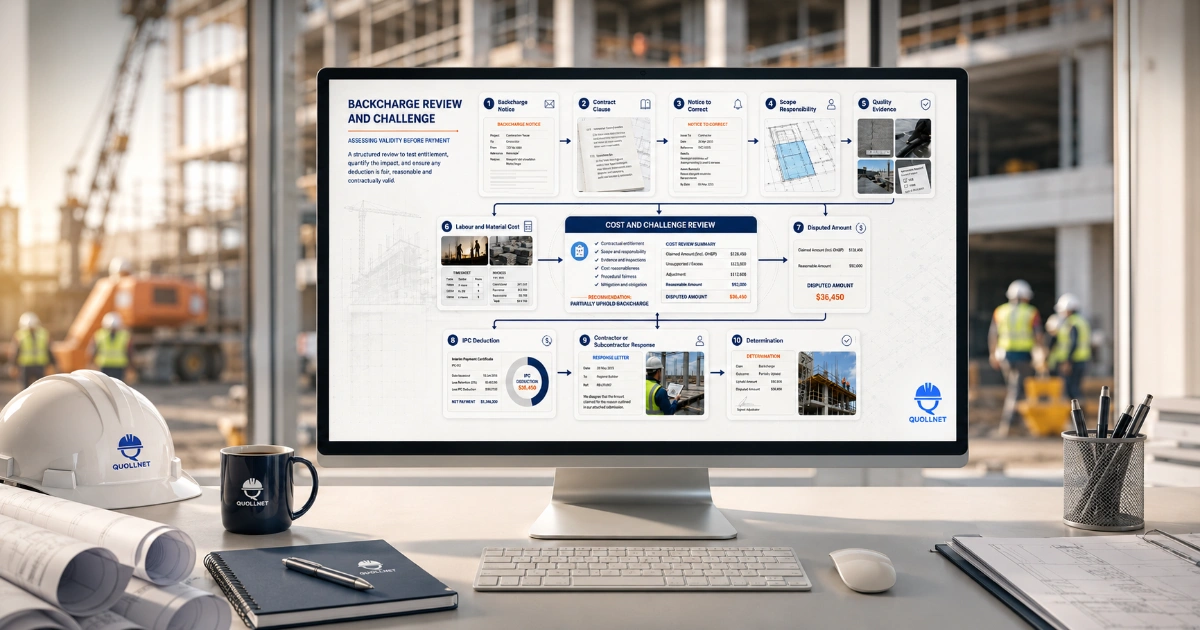

Once a backcharge has been raised, the commercial team must decide whether any amount can properly be deducted from the Subcontractor’s current payment. An entry in a construction Backcharge Log for IPC deductions or an internal approval does not, by itself, establish contractual entitlement to deduct that amount.

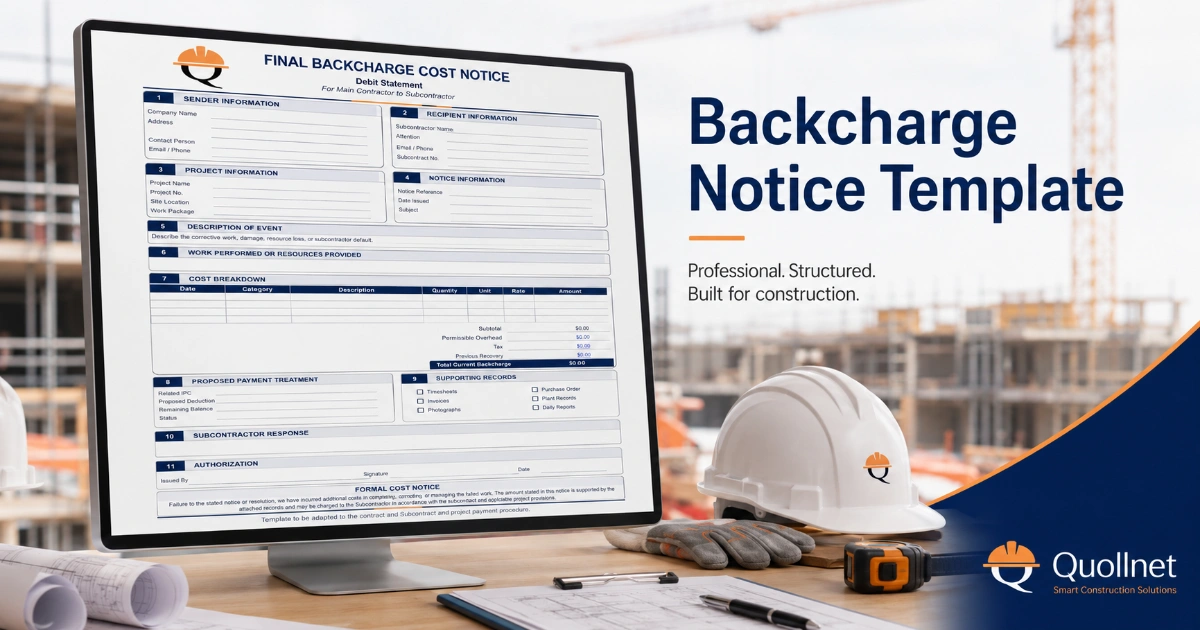

Need to issue the underlying notice first?

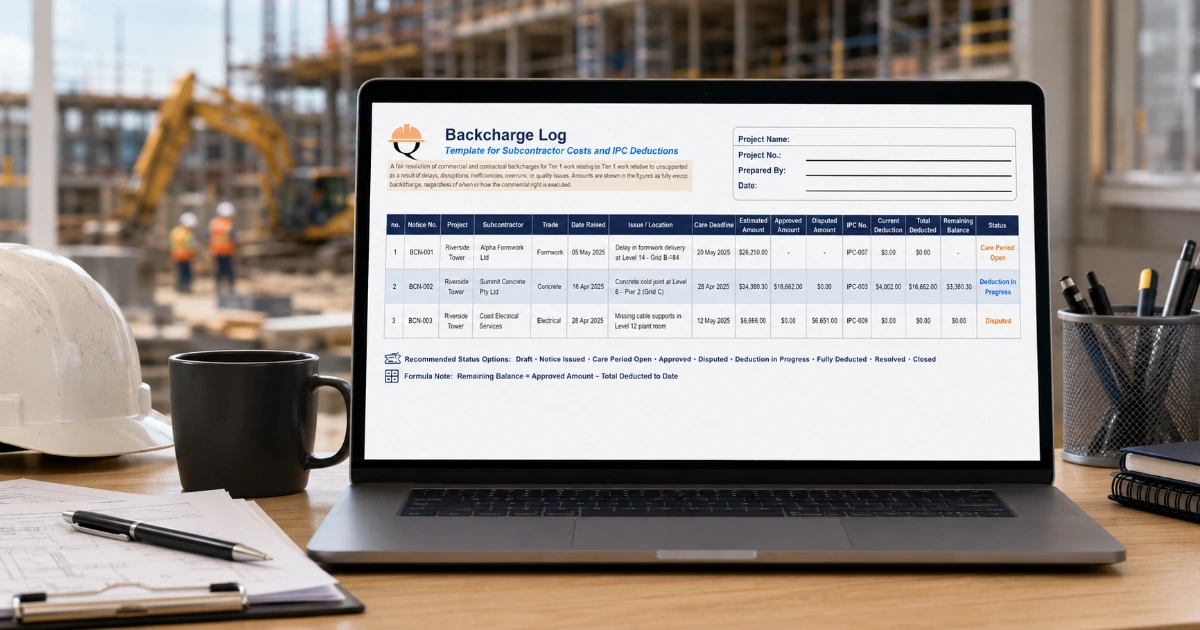

Use the Backcharge Notice Template to identify the default, correction period, possible work by others, and proposed cost recovery. Record the notice and every later deduction in the Construction Backcharge Log.

What Is a Subcontractor IPC?

A Subcontractor Interim Payment Certificate, or IPC, is the periodic assessment used to calculate what is currently payable under a subcontract. Depending on the project and jurisdiction, it may instead be called an interim valuation, progress claim, payment application, subcontract payment assessment, or payment certificate.

In some projects, the Subcontractor submits an application and the Main Contractor prepares the assessment. In others, the document itself is called an IPC. It commonly records:

- gross value of completed work;

- approved Variations;

- permitted materials on or off site;

- retention;

- advance-payment recovery;

- previously certified amounts;

- other contractual deductions;

- backcharges;

- the net current amount due.

A backcharge should be presented as a distinct commercial adjustment. It should not be hidden by reducing measured quantities, changing agreed rates, removing unrelated approved work, or increasing construction retention.

When May a Backcharge Be Deducted?

Before deducting a backcharge from a Subcontractor IPC, the Main Contractor should normally verify:

- the contractual basis for recovery or set-off;

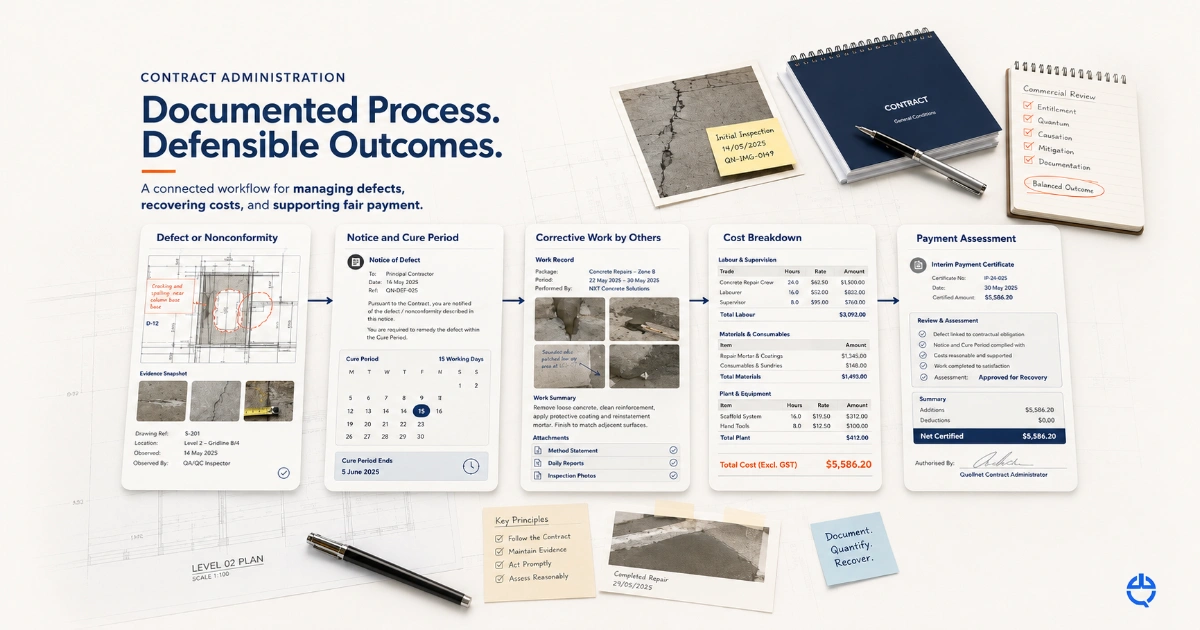

- the instruction, Defect notification, NCR, or Notice to Correct issued before engaging others;

- the Subcontractor’s access and opportunity to correct the work, where applicable;

- the right to use supplementary resources or engage another party;

- responsibility, causation, and scope allocation;

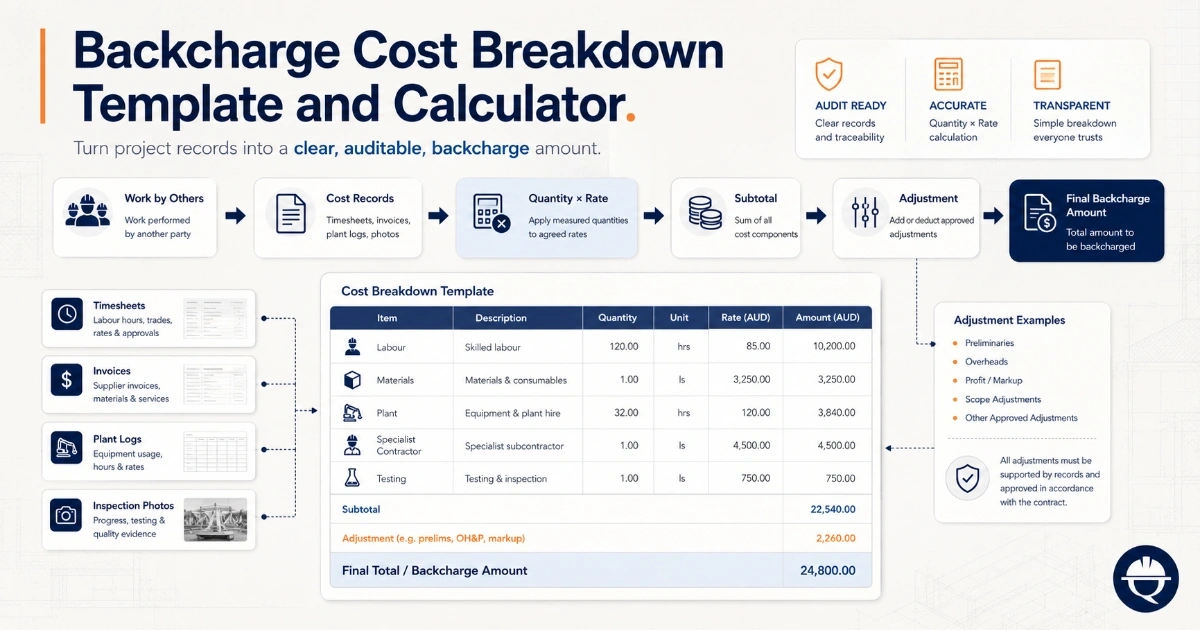

- actual labour, material, plant, testing, and specialist records;

- internal commercial approval;

- any required agreement, assessment, certification, or determination;

- the Subcontractor’s response or dispute;

- the payment notice, pay-less notice, set-off, or other payment procedure.

The following statuses should not be treated as interchangeable:

- Potential backcharge: a warning that corrective cost may arise.

- Estimated backcharge: a preliminary value before complete records are available.

- Actual backcharge cost: an evidenced cost incurred or otherwise assessable under the Subcontract.

- Internally approved backcharge: an amount authorized through the Main Contractor’s internal process.

- Agreed or determined amount: an amount accepted by the Subcontractor or established through the contractual mechanism.

- Current IPC deduction: the portion permitted to be applied in the present payment cycle.

Internal approval confirms that the Main Contractor is commercially prepared to proceed. It does not necessarily prove liability, valuation, or the right to deduct from the current IPC.

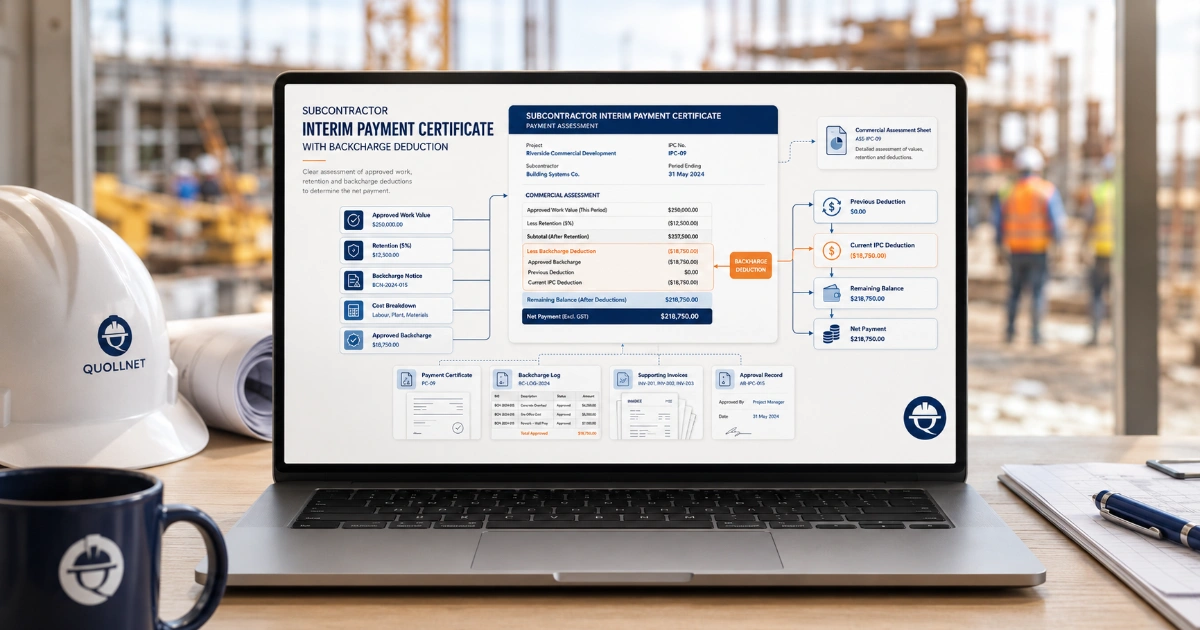

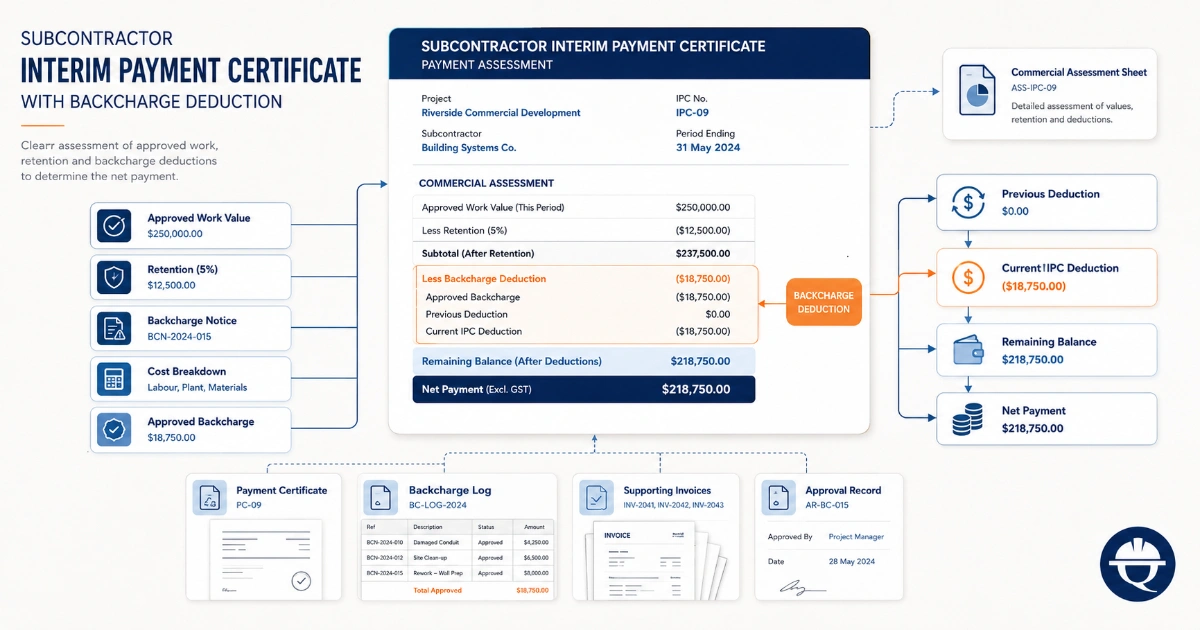

How Should the Backcharge Deduction Appear in the IPC?

Show the backcharge as a separate and identifiable line. Each line should state the Backcharge Notice number, short description, related clause, approved or assessed value, previous deductions, current deduction, remaining balance, status, cost-breakdown reference, and any payment-notice reference.

Where several backcharges apply, list each separately or attach a detailed schedule reconciled to one total deduction line. Do not combine unidentified corrective costs into a single unexplained “miscellaneous deduction.”

Worked IPC Calculation

The $7,500 should also reconcile with the Backcharge Notice, cost breakdown, approval record, Backcharge Log, and payment notice or assessment.

Calculating the Remaining Backcharge Balance

Track the approved amount separately from amounts already recovered:

Remaining balance = Approved backcharge − Total deducted to date

For example, if the approved backcharge is $18,000, $6,000 was deducted in IPC 7, and $5,000 is deducted in IPC 8:

- approved backcharge: $18,000;

- deducted in IPC 7: $6,000;

- deducted in IPC 8: $5,000;

- total deducted to date: $11,000;

- remaining balance: $7,000.

The current deduction should not exceed the remaining approved balance or the amount contractually available for deduction in that payment cycle.

When the Backcharge Exceeds the Current Amount Due

If the current IPC is smaller than the backcharge, the Main Contractor should not assume that the full balance can automatically be taken from retention or another account. Depending on the Subcontract, possible treatments may include:

- a partial deduction in the current IPC;

- carrying the remaining balance to later IPCs;

- a final-account adjustment;

- set-off against other payments where expressly permitted;

- recovery as a debt;

- a separate claim or dispute procedure.

The outstanding balance should remain open in the Backcharge Log until it is recovered, reversed, settled, transferred, or formally closed.

Disputed Backcharges and Payment Notices

A disputed amount should remain visible. The IPC schedule may separately record the claimed amount, internally approved amount, accepted amount, disputed amount, current deduction, amount held pending determination, and remaining balance.

Marking an amount as disputed does not automatically prevent deduction, and internal approval does not automatically permit it. The Subcontract and applicable payment law determine whether the amount may be withheld in the current cycle.

The Subcontractor may challenge contractual entitlement, responsibility, scope, notice, correction opportunity, access, causation, correction method, actual cost, labour hours, rates, overhead, profit, betterment, duplicate recovery, or the timing and basis of the payment notice. See how to challenge an improper backcharge.

Contract and Payment Procedures

- FIDIC: the relevant procedure may involve notice, an Employer’s claim, Engineer review or determination, and treatment in the payment certificate.

- AIA: correction costs, withholding, certification, and Claims may be separate stages.

- NEC: notified Defects, correction periods, cost assessment, and payment mechanisms must be followed.

- JCT: substantive entitlement may need to be supported by a compliant payment notice or pay-less notice.

Review the applicable FIDIC, AIA, NEC, or JCT backcharge guide. Contract editions, amendments, jurisdiction, and notice deadlines matter.

Where a payment notice or pay-less notice is required, it should identify the amount considered due and the basis of calculation, including the backcharge deduction. Missing or late notice may affect the amount payable in that cycle even where the underlying correction-cost claim can still be pursued separately. See Timely Notices in Construction.

Reversals, Credits, and Later Adjustments

A backcharge may later be reduced, rejected, withdrawn, settled, partly accepted, transferred to another responsible party, covered by insurance, found to include betterment, duplicated, or reversed through determination or dispute resolution.

Any correction should appear transparently in the next IPC. For example:

- previously deducted: $10,000;

- final agreed backcharge: $6,500;

- credit due to the Subcontractor: $3,500.

Show the $3,500 as a separate credit or backcharge reversal. Do not silently return it by increasing quantities, rates, or unrelated Variation values. Update both the IPC schedule and Backcharge Log.

Reconcile the IPC with the Backcharge Log

Every deduction should reconcile with the commercial record. The Backcharge Log should show:

- notice number and description;

- approved and disputed amounts;

- previous and current deductions;

- total deducted to date;

- remaining balance;

- related IPC and payment-notice reference;

- status, reversal, settlement, and closure date.

Documents to Check Before Deduction

- executed Subcontract and relevant clause;

- site instruction, Defect notification, NCR, or Notice to Correct;

- evidence of delivery and correction deadline;

- Subcontractor response;

- photographs, inspection records, and test results;

- labour timesheets and plant records;

- material invoices and specialist quotations or invoices;

- supported Backcharge Cost Breakdown and Calculator;

- internal approval and Backcharge Log entry;

- current IPC assessment;

- payment notice, pay-less notice, agreement, or determination where required.

Common IPC Backcharge Deduction Errors

- deducting an estimated amount as though it were final;

- hiding the deduction in measured quantities or agreed rates;

- using retention as a substitute for a specific backcharge;

- deducting without a notice or cost-breakdown reference;

- deducting more than the approved remaining balance;

- repeating the same amount in multiple IPCs;

- failing to show previous deductions and remaining balance;

- ignoring the disputed status of an amount;

- adding unsupported overhead, administration, or profit;

- deducting before the correction period expires;

- charging work caused by another trade or additional scope;

- missing a required payment or pay-less notice;

- failing to credit a rejected or reduced backcharge.

Conclusion

A backcharge deduction from a Subcontractor IPC should be separately identified, supported, approved, reconciled, and processed through the correct contractual payment mechanism. Liability for the event, valuation of the corrective cost, and the right to deduct it from the current IPC must each be checked.

Use the Backcharge Notice Template before transferring corrective work, the cost calculator to substantiate the amount, and the Backcharge Log to track deductions, remaining balances, disputes, credits, and closure.

This article provides general construction contract-administration guidance and is not legal advice. The executed Subcontract, amendments, governing law, payment procedure, and project facts control.

REFERENCES

FIDIC Guidance on Notices and Notice to Correct

FIDIC: Determination of Costs Incurred in Remedying Defects

AIA Contract Documents: Right to Carry Out Corrective Work and Recover Costs

AIA A201–2017 General Conditions Summary

AIA G703S–2017 Contractor–Subcontractor Payment Continuation Sheet

NEC: Dealing with Uncorrected Defects under the Engineering and Construction Subcontract

NEC: Defining and Managing Defects and Liability for Not Correcting Them