Prime Cost Sums in Construction Contracts: Hidden Risks and Pricing Strategies

Prime Cost (PC) sums adjust material supply allowances in construction contracts, but they do not adjust execution risk. This guide explains how PC items affect contractor margin, how BOQ structure changes exposure, and where to place overhead and profit to avoid unintended losses during material selection.

Prime Cost (PC) sums are commonly used in construction contracts to allow flexibility in selecting materials later in the project. While they appear straightforward, they introduce hidden pricing risks that can affect contractor margin, wastage exposure, and defects liability obligations.

Understanding how to structure and price PC items correctly—especially in Bills of Quantities (BOQs)—is essential for protecting both contractor and employer from unintended financial consequences.

This guide explains how PC sums work in practice, why they create hidden risk, and how to decide where overhead and profit (OH&P) should be placed when pricing them.

What Is a Prime Cost Sum?

A Prime Cost (PC) sum is an allowance included in the contract for materials that will be selected later by the Architect/Engineer or employer.

Prime Cost sums are recognized across major contract frameworks including FIDIC, AIA contract forms, and RICS measurement guidance, where they are used to manage material selections that cannot be finalized at tender stage.

Unlike provisional sums, which adjust scope uncertainty, prime cost sums mainly adjust material selection uncertainty.

The allowance typically covers supply only, while installation is priced separately by the contractor.

Typical PC items include:

-

ceramic tiles

-

sanitary fixtures

-

light fittings

-

timber flooring

-

doors and ironmongery

-

architectural finishes

Once the final material is selected, the contract sum is adjusted to reflect the actual supply cost.

However:

PC adjustments usually compensate material price only—not execution exposure.

Why Prime Cost Sums Create Hidden Contractor Risk

PC sums adjust supply value but usually do not adjust execution risk.

They typically do not compensate changes in:

-

wastage value

-

handling sensitivity

-

storage requirements

-

installation productivity

-

supervision effort

-

protection requirements

-

replacement obligations during the defects liability period (DLP)

As material value increases, these risks increase—even if installation rates remain unchanged.

This makes PC sums one of the most misunderstood pricing mechanisms in BOQ contracts.

Why Employers Use Prime Cost Sums

Employers and consultants use Prime Cost sums to keep the tender moving when final finishes, fixtures, or specialist materials are not yet fully selected. This gives the design team flexibility and can avoid delaying procurement of the main works package. However, the employer should understand that a PC sum does not eliminate risk; it only postpones final material selection. If the allowance is unrealistic, or if selections are made late, the project may still face cost growth, coordination issues, approval delays, and pressure on programme.

Prime Cost Sums Create Selection and Supply-Chain Risk

Prime Cost sums are not only pricing allowances. They also create selection and supply-chain risk. When the final material is chosen later by the architect, engineer, or employer, the contractor may still face uncertainty in supplier lead time, sample approvals, procurement timing, delivery sequencing, storage conditions, handling requirements, and coordination with installation activities. In other words, the contract may carry an allowance for material value, but the project may still be carrying uncertainty in how that material will actually be selected, sourced, and absorbed into the works.

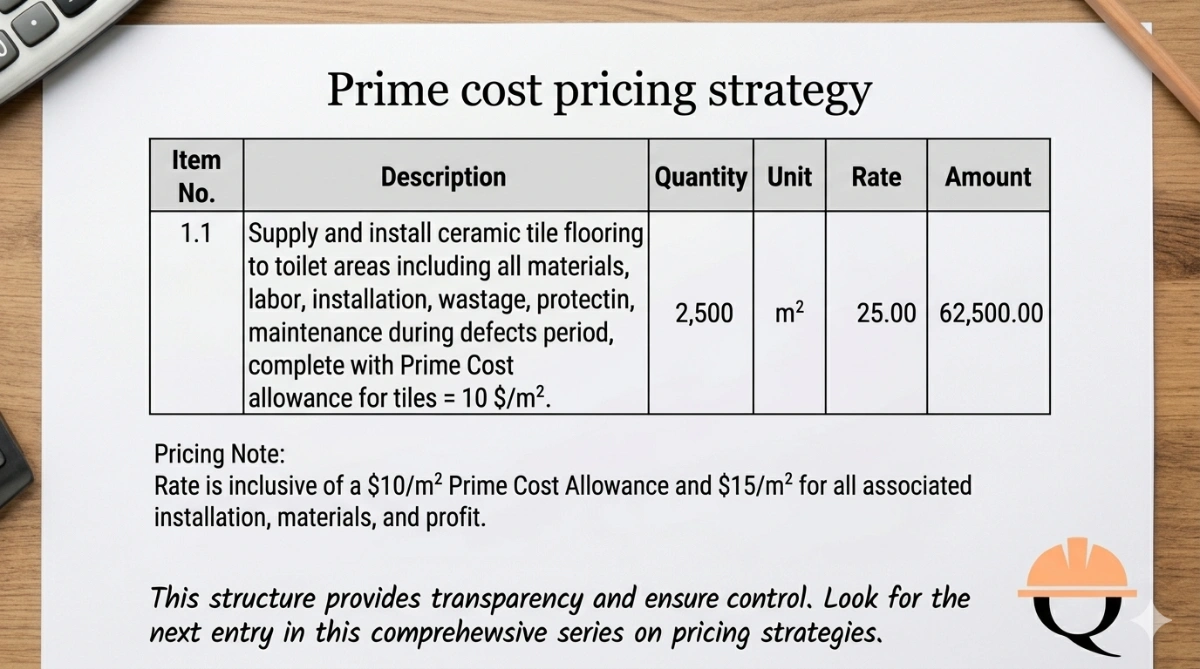

Real Example: Ceramic Tile PC Allowance (Composite BOQ Structure)

Consider the following BOQ wording.

Composite format (single-line PC structure)

Supply and install ceramic tile flooring to toilet areas including supply, installation, adhesive, accessories, transportation, cutting, wastage, protection, and maintenance during the defects liability period, complete as per drawings and specifications, with Prime Cost allowance for tiles = 10 $/m².

| Quantity | Unit | Rate | Amount |

|---|---|---|---|

| 2,500 | m² | 25 | 62,500 |

Here:

Total rate includes:

-

installation

-

accessories

-

wastage

-

OH&P

-

PC allowance

If selected tiles cost 18 $/m²:

Adjustment = +8 × 2,500

Installation pricing remains unchanged.

This structure generally protects contractor margin better than split PC structures.

Alternative Example: Split PC BOQ Structure

Some BOQs separate supply allowance from installation works.

Item 1 — PC Material

Prime Cost allowance for supply of ceramic floor tiles to toilet areas as selected by the Architect/Engineer.

| Quantity | Unit | Rate | Amount |

|---|---|---|---|

| 2,500 | m² | 10 | 25,000 |

Item 2 — Installation Works

Installation of ceramic floor tiles including adhesive, accessories, cutting, wastage, transportation, supervision, protection, testing, and maintenance during defects liability period, complete as per drawings and specifications.

| Quantity | Unit | Rate | Amount |

|---|---|---|---|

| 2,500 | m² | 15 | 37,500 |

This structure introduces a key pricing decision:

Where should overhead and profit be placed?

Why the Split Structure Creates Margin Risk

If overhead and profit are included inside the PC item instead of the installation item, contractor margin may reduce automatically when cheaper materials are selected.

Original Tender (Markup Hidden Inside PC Item)

| Component | Value ($/m²) |

|---|---|

| Base PC allowance | 10 |

| Contractor OH&P inside PC | 2 |

| Tendered PC rate | 12 |

| Installation item | 15 |

Now assume the Architect/Engineer selects tiles costing 5 $/m².

Post-Selection Adjustment

| Component | Value ($/m²) |

|---|---|

| Selected tile supply cost | 5 |

| Adjusted proportional OH&P | 1 |

| Adjusted PC rate | 6 |

Result:

The contractor loses 1 $/m² of margin compared to the original tender assumption.

If OH&P had been placed in the installation item instead, the margin would remain unchanged.

A Second Example: Sanitary Ware PC Allowance

PC exposure increases significantly when materials are expensive.

Example wording:

Supply and install wash basin including brackets, fixing accessories, sealants, connection to water supply and drainage, testing, protection, and maintenance during defects liability period, complete as per drawings and specifications, with Prime Cost allowance for basin = 120 $/No.

If the selected basin costs:

400 $

Replacement during DLP becomes substantially more expensive.

Yet installation pricing remains unchanged unless the contract explicitly allows adjustment.

Wastage and Defects Liability Period Exposure

PC sums adjust supply value only—not lifecycle exposure.

Higher-value materials increase:

-

breakage risk

-

replacement cost

-

storage requirements

-

handling sensitivity

-

protection effort

-

supervision complexity

For example:

Replacing a cracked 5 $ tile during DLP is negligible.

Replacing a 100 $ tile is not.

However, installation pricing usually remains unchanged.

This is one of the most overlooked risks in PC pricing.

Two Common BOQ Structures Compared

| Structure | Adjustment Risk | Margin Stability |

|---|---|---|

| Composite PC item | Low | High |

| Split PC item | Medium | Depends on markup placement |

| Split PC with markup inside PC | High | Low |

As a general rule:

Avoid placing OH&P inside adjustable PC items unless higher-value selections are expected.

Decision Strategy: Where Should OH&P Be Placed?

The correct placement of overhead and profit depends on expected material selection direction.

Use the following workflow.

Prime Cost OH&P Placement Strategy (Selection Direction Flowchart)

This decision framework helps contractors balance margin protection against potential upside when materials exceed PC allowances.

PC Pricing Decision Workflow

Step 1 — Is the BOQ composite or split?

Composite item:

Margin is generally stable.

Split item:

Continue to Step 2.

Step 2 — Is the final material selection likely to exceed the PC allowance?

Yes:

Place part of OH&P inside PC item (possible upside)

No:

Place OH&P inside installation item (protect margin)

Uncertain:

Place OH&P inside installation item (lowest risk strategy)

PC Sum Pricing Decision Tree (Composite vs Split Logic)

Decision Table for Fast Pricing Strategy Selection

| Expected Selection Outcome | Recommended OH&P Placement | Risk Level |

|---|---|---|

| Higher than PC allowance | Inside PC item | Moderate |

| Near PC allowance | Split between both | Medium |

| Lower than PC allowance | Inside installation item | Low |

| Unknown | Inside installation item | Lowest |

This table is especially useful during tender pricing reviews.

Project Type Matters When Pricing PC Items

Material selection direction often depends on project type.

| Project Type | Likely Selection Outcome |

|---|---|

| low-cost housing | below PC allowance |

| mid-range residential | near allowance |

| luxury residential tower | above allowance |

| 5-star hotel | above allowance |

Estimators should align OH&P placement strategy with expected specification upgrades or value engineering risk.

Practical Strategy for Structuring PC BOQ Items

When pricing PC items:

Separate fixed installation costs from material-sensitive costs

Avoid embedding margin inside adjustable PC allowances unless justified

Consider wastage exposure relative to material value

Evaluate replacement exposure during defects liability period

Assess likely selection direction based on project type

If uncertain:

Place overhead and profit inside the fixed installation portion rather than the adjustable PC allowance.

Key Takeaway

Prime Cost sums adjust material price but not execution risk.

Contractors should structure BOQ rates carefully to avoid unintended margin erosion when final selections differ from tender assumptions.

Correct placement of overhead and profit inside PC structures is one of the simplest and most effective ways to protect pricing stability in construction contracts.